Table of Content

- What ezzocard.com is

- How the platform works

- Types of services offered

- How users typically use it

- Pricing and fee reality

- Review analysis: Trustpilot and other public review platforms

- What users praise

- Trust scores and risk indicators

- Comparison with alternatives

- Evidence-based strengths and weaknesses

- Final verdict

What ezzocard.com is

Ezzocard markets virtual prepaid Visa and Mastercard cards for online payments, with a strong emphasis on anonymity, crypto payments, and worldwide use. The current official public site says Ezzocard.com is now Ezzocard.finance, and describes the product as virtual prepaid cards issued by banks in the United States and Canada. The FAQ says the cards are prepaid, non-reloadable, and carry no cardholder personal data, which the company frames as an anonymous payment method. (ezzocard.finance)

In practical terms, the service is selling single-load virtual payment cards that users buy with crypto, receive by email, and then use at merchants that accept Visa or Mastercard prepaid cards. The company says delivery is usually within 2 to 5 minutes, requires only an email address, and supports BTC, ETH, and USDT for payment.

How the platform works

The basic flow is simple:

1. Pick a card type and denomination

2. Pay in cryptocurrency

3. Receive the virtual card details by email

4. Use the card online at supported merchants

That flow is spelled out on Ezzocard’s own “virtual credit card” and purchase pages. The company also says some cards can be registered to a billing address, some do not require registration, some support Google Pay / Apple Pay, and some are restricted by region or IP rules.

That last point matters. The official product descriptions say several card types can be blocked if used from the wrong region or IP. For example, some products say to use a U.S. or EU IP, while one Lime variant says to use a U.S. IP only or risk the issuer blocking the card with no possibility of a refund. That is a major operational risk, and it means this is not a plug-and-play consumer product in the same way as mainstream fintech virtual cards.

Types of services offered

The service is broader than a single anonymous card. From the official pages, Ezzocard currently offers:

| Service area | What surfaced |

| Virtual prepaid Visa and Mastercard cards | USD and CAD cards in multiple variants and denominations |

| Anonymous crypto-funded checkout | BTC, ETH, USDT accepted |

| Address registration / AVS support on some cards | Some cards can be linked to U.S. or Canadian billing addresses |

| Balance / statement tools | Mentioned in public review snippets |

| Free trial card | New-user offer with a $5 cap and 30-day validity |

| Card recharge service | Ezzocard says users can add funds to any credit card number through a separate recharge tool |

The strongest official evidence is for the prepaid cards themselves, the crypto checkout flow, the free test card, and the non-reloadable card design. The “card recharge” feature is also described on the official site, but that service needs more caution because it is less well known and not well documented outside the company’s own pages.

How users typically use it

The most common use cases that surfaced were:

1. online purchases where users do not want to expose their main bank card

2. one-off payments and testing

3. subscriptions or merchant verification attempts

4. privacy-oriented transactions funded by crypto

5. cross-border purchases where local payment methods are inconvenient

The company itself markets the cards for anonymous online shopping and verification. Trustpilot snippets mention use on Apple services, Google, Amazon, hosting, VPNs, and subscriptions. Reddit comments also refer to Ezzocard as a privacy-oriented prepaid card option, though not the cheapest one.

One important limitation is that Ezzocard’s own FAQ says its prepaid cards are generally not reloadable and do not support recurring payments as a rule, even though individual card types can differ. So the typical use case is closer to a controlled, one-time or limited-use payment instrument than a full-featured digital banking card.

Pricing and fee reality

This is one of the clearest problem areas. Ezzocard’s prices often sit well above the value loaded onto the card. Its discount-program page exposes regular prices for many cards, and the premiums are substantial. Examples from the official pricing table:

| Example card | Loaded value | Listed price | Premium over value |

| Violet Visa | $100 | $135.99 | 36.0% |

| Red Mastercard | $100 | $136.99 | 37.0% |

| Orange Visa | $100 | $141.99 | 42.0% |

| Gold Visa / Mastercard | $100 | $149.99 | 50.0% |

| Brown CAD | C$100 | C$99.99 | about 0% |

| Teal CAD | C$100 | C$89.99 | below face value in this surfaced table |

Those prices come directly from Ezzocard’s own discount-program page. The product pages also mention extra conditions such as 2.5% non-CAD transaction fees for some CAD cards and monthly fees on some products after a certain time.

The fee structure is not uniformly bad, but it is clearly not cheap. On Trustpilot and third-party commentary, “works but expensive” is a recurring theme. That matches the official price tables much more than the marketing language does.

I also made a chart from the official pricing examples: Ezzocard official price premium graph

Review analysis: Trustpilot and other public review platforms

Trustpilot

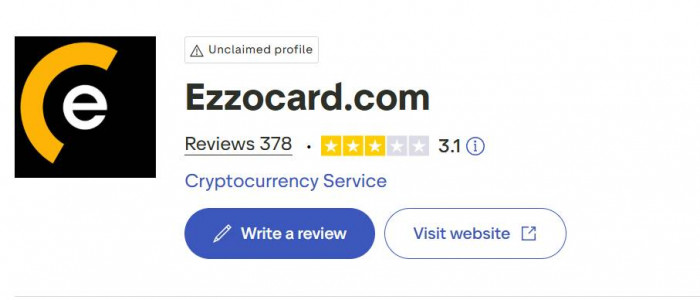

Trustpilot is the biggest public review pool I found. The current surfaced page shows 378 reviews and a 3.1 / 5 TrustScore. The rating mix is highly polarized: 65% 5-star and 28% 1-star, with very little in the middle. That is a classic “works great for some, fails badly for others” profile. Trustpilot also places a warning on the page saying the company may be associated with high-risk investments.

Using Trustpilot’s displayed percentages and review count, the approximate distribution looks like this:

| Rating | Share | Approx. reviews |

| 5-star | 65% | ~246 |

| 4-star | 5% | ~19 |

| 3-star | 1% | ~4 |

| 2-star | 1% | ~4 |

| 1-star | 28% | ~105 |

That estimate is derived from the Trustpilot percentages on the surfaced page.

I turned that into a chart here: Trustpilot ratings distribution graph

Scamadviser

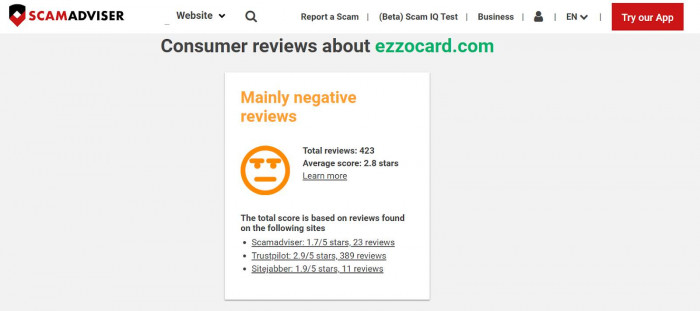

Scamadviser gives a split signal. On one hand, it says Ezzocard is “very likely not a scam but legit and reliable” and notes positives such as a valid SSL certificate, site age, and DNSFilter safety. On the other hand, the same page also says the site has received mainly negative reviews, cites low traffic rank, and aggregates public reviews into an overall 2.8 / 5 average across 423 reviews from Scamadviser, Trustpilot, and Sitejabber.

That combination matters. Scamadviser is not saying “safe and loved.” It is closer to saying, “probably a real site, but public satisfaction is not strong.”

Scam Detector

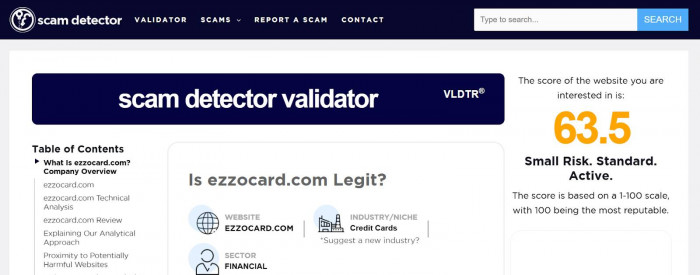

Scam Detector gives Ezzocard a 63.5 / 100 score and labels it “Small Risk. Standard. Active.” It also notes a valid HTTPS connection, no blacklist detection, and an old domain creation date, but still says the business poses potential risk.

Sitejabber

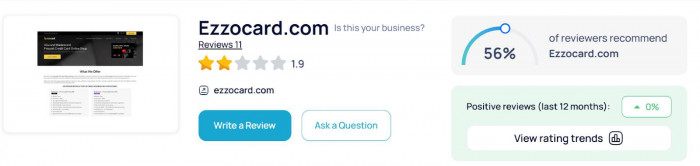

Sitejabber is much more negative. It shows 1.9 / 5 from 11 reviews, says most customers are generally dissatisfied, and lists 44% 1-star and 44% 5-star, again reflecting a polarized experience pattern.

What users praise

The positive side of the feedback is fairly consistent. Users who like Ezzocard usually mention:

1. fast card delivery

2. ability to pay with crypto

3. privacy and anonymity

4. success at some mainstream merchants

5. simple setup

Trustpilot snippets mention instant delivery, working cards on Apple services, Amazon, Google, hosting, and VPN services. Reddit also has users describing it as functional, though expensive.

So the bull case is real: some customers clearly do receive working cards and use them successfully. This is why I would not label it a flat-out fake service.

Trust scores and risk indicators

Here is the cleanest summary of the public trust signals I found:

| Source | Signal |

| Trustpilot | 3.1 / 5 from 378 reviews, with a 65% 5-star and 28% 1-star split |

| Scamadviser | “Very likely not a scam,” but also “mainly negative reviews” and 2.8 / 5 aggregated review average |

| Scam Detector | 63.5 / 100, “Small Risk. Standard. Active.” |

| Sitejabber | 1.9 / 5 from 11 reviews |

| Reddit / forums | Mixed, often functional but expensive; repeated warnings about spoof domains |

These sources do not point in the same direction. That is the key insight. The website itself looks longstanding and technically live, but the user-experience layer is unstable and highly mixed.

Comparison with alternatives

Ezzocard makes the most sense to compare with privacy-focused or virtual-card services, not normal bank accounts.

| Service | Funding model | Identity posture | Pricing posture | Risk profile vs Ezzocard |

| Ezzocard | Crypto-funded prepaid cards | Very high anonymity | High card premium on many products | Higher acceptance and trust risk |

| Privacy.com | Linked bank / debit funding | Mainstream U.S. consumer identity model | Free personal tier, paid upgrades | Lower anonymity, stronger mainstream trust |

| IronVest | Subscription with virtual cards | Identity-protective, but mainstream service model | $39/year Plus, up to 35 virtual cards | More structured, less anonymous, stronger brand trust |

| Revolut virtual / disposable cards | App-based fintech account | Full-account model, not anonymous | Disposable cards available in-app | Lower anonymity, much stronger mainstream infrastructure |

Privacy.com’s public pages show a free personal plan, 12 new cards per month, spend limits, single-use and merchant-locked cards, with foreign transaction fees on lower tiers. IronVest publicly advertises virtual cards inside a security suite for $39/year on Plus. Revolut promotes virtual and disposable cards created inside its app, including single-use behavior for safer one-time purchases.

That comparison makes Ezzocard’s niche clearer. Its real differentiator is anonymity plus crypto funding, not low cost or trust. Mainstream alternatives usually win on transparency, ecosystem quality, and merchant acceptance, while losing on anonymity.

Evidence-based strengths and weaknesses

Strengths

| Strength | Evidence |

| Real functioning product for at least some users | Many positive Trustpilot snippets and older Reddit/forum mentions of successful use |

| Fast issuance | Official site says 2 to 5 minute delivery |

| Crypto-funded checkout | Official purchase page |

| Multiple card types and regions | Official catalog shows USD and CAD options, AVS and regional variants |

| Good for privacy-first buyers | Official FAQ emphasizes anonymity and no personal data |

Weaknesses

| Weakness | Evidence |

| Very mixed customer outcomes | Trustpilot polarization and weak Sitejabber score |

| High premiums over card value | Official pricing table |

| Merchant acceptance uncertainty | Company replies say not all merchants accept prepaid cards |

| Domain confusion / spoof risk | Reddit warnings about lookalike domains |

| Some products have harsh IP / region rules | Official card descriptions warn of blocking and no refund |

| Refund limitations | Official FAQ says purchases are generally non-refundable once delivered |

Final verdict

Based on the evidence, Ezzocard is best described as legitimate but risky.

It does not look like a simple fake website. There is a long-lived domain trail, functioning official pages, technical card documentation, many public reviews, and enough credible user reports of successful use to show a real service exists.

But it also does not look like a dependable mainstream financial product. The public review profile is too polarized, the pricing premiums are often steep, the merchant-acceptance risk is real, support complaints recur, and brand spoofing around the Ezzocard name adds another layer of danger. (Trustpilot)

My bottom-line classification:

| Verdict category | Assessment |

| Legitimate service exists | Yes |

| Low-risk / mainstream reliable | No |

| Good value | Mixed to poor on many cards |

| Suitable for careful test use | Possibly |

| Suitable for large or important payments | No |

So the most honest answer is: Ezzocard is not obviously a scam, but it is risky and unreliable enough that I would only use it for a small, disposable test payment, never for critical spending or a large balance.